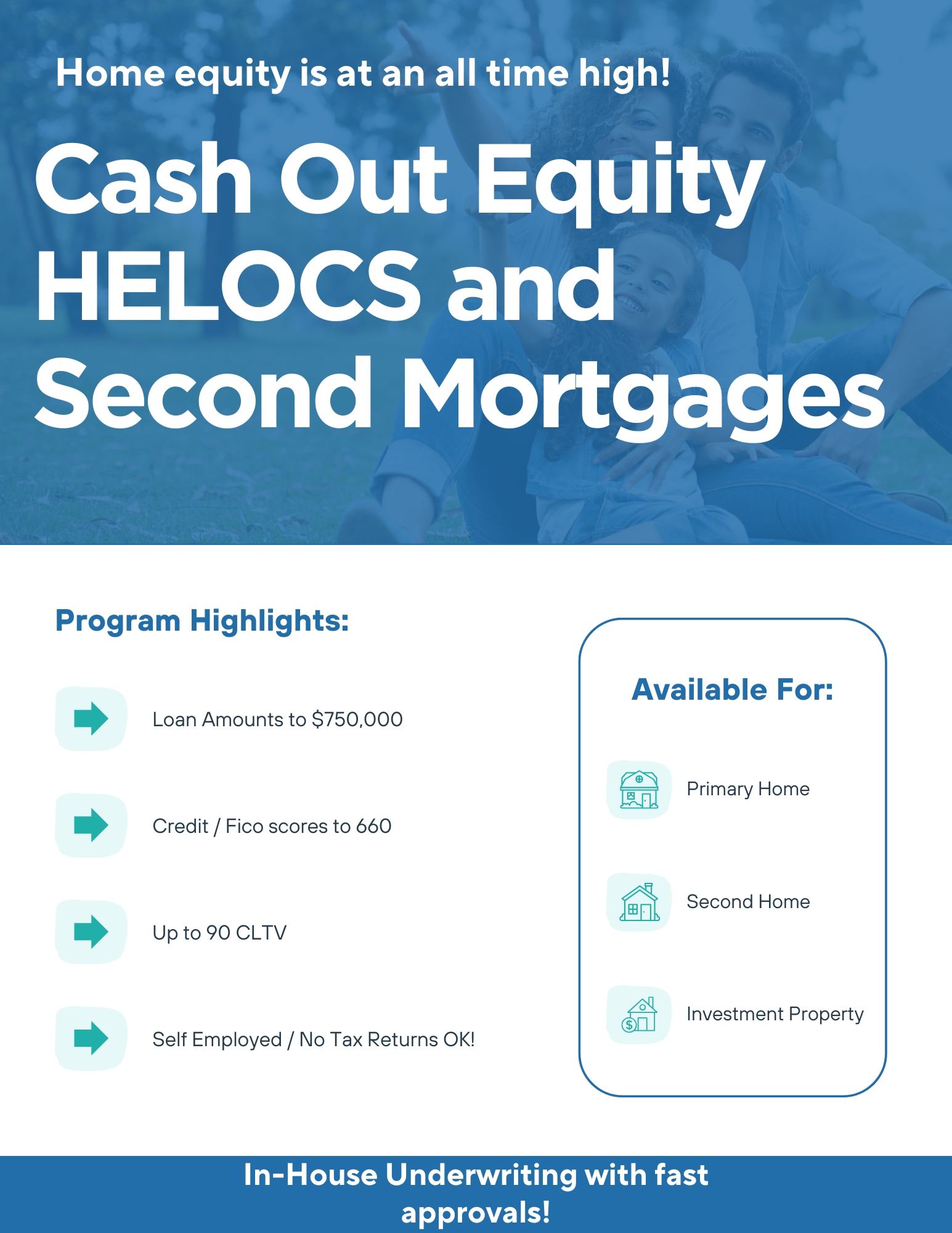

A Home Equity Line of Credit (HELOC) comes with several benefits:

Flexibility: You can borrow only what you need, pay it back, and borrow again, as long as you stay within your credit limit. -

Lower Interest Rates: Compared to credit cards or personal loans, HELOCs typically have lower interest rates because they're secured by your home. -

Access to Funds: Use the money for a wide variety of purposes, like home improvements, education costs, debt consolidation, or emergencies. - Potential Tax Benefits: In some cases, the interest on a HELOC may be tax-deductible if the funds are used for home-related expenses (consult a tax advisor for details).

The key is that a HELOC gives you financial flexibility while leveraging the equity you've built up in your home. It can be a smart option, but it’s important to borrow responsibly since your home serves as collateral. Let me know if you'd like more details or advice!

A fixed second mortgage loan has several advantages:

Stable Payments: The fixed interest rate ensures that your monthly payments remain consistent over the life of the loan, which helps with budgeting and financial planning.

Access to a Lump Sum: You receive a one-time payment upfront, making it ideal for large expenses like home renovations, medical bills, or debt consolidation.

Lower Interest Rates: Since it's secured by your home, the interest rates are typically lower than unsecured loans or credit cards.

Potential Tax Benefits: In some cases, the interest paid on the loan might be tax-deductible if the funds are used for home-related expenses (consult a tax advisor for specific advice).

Predictability: The fixed term and interest rate provide a clear timeline for repayment, reducing uncertainty. This type of loan can be a great choice if you have a specific expense in mind and want the security of predictable payments. Let me know if you'd like to dive deeper into the details!